The Nigeria–Morocco Gas Pipeline is one of the most ambitious energy infrastructure projects ever proposed on the African continent.

The project is designed to connect Nigerian gas resources to West African countries, Morocco and potentially European markets through a vast Atlantic corridor. If completed, it could reshape energy security, industrial development and regional integration across more than a dozen countries.

The scale is extraordinary.

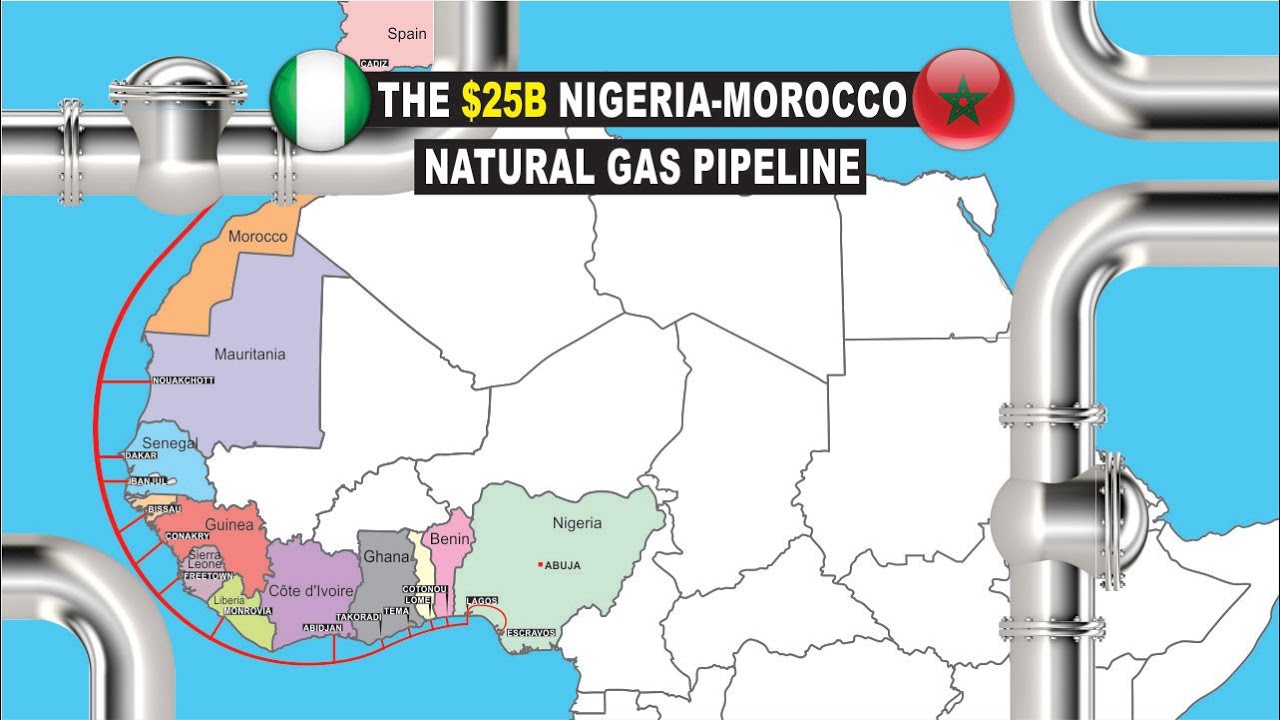

The pipeline is expected to run roughly 6,800 to 6,900 kilometres, with a maximum capacity of around 30 billion cubic metres of gas per year. It has been widely estimated at about $25 billion, making it one of Africa’s most complex cross-border infrastructure projects. (Reuters, Maritime Professional)

For Morocco, the project is not only about gas.

It is about energy security, Atlantic strategy, African integration, industrial competitiveness and the country’s long-term role as a bridge between West African resources and European demand.

But ambition is not execution.

The real question is whether a project of this scale can move from diplomatic alignment and feasibility studies into financing, construction, offtake agreements and operational delivery.

An Atlantic Energy Corridor

The Nigeria–Morocco Gas Pipeline is designed as an Atlantic energy corridor linking Nigeria to Morocco through West Africa.

The project would pass along the Atlantic coast, connecting or serving countries across the region before reaching Morocco and linking into wider gas infrastructure.

Its strategic logic is clear.

Nigeria has some of Africa’s largest gas reserves. West African countries need more reliable energy access. Morocco wants to diversify its energy mix and strengthen its position as a regional energy platform. Europe continues to look for diversified gas supply routes.

That gives the pipeline a multi-layered function.

It is not just a pipeline.

It is a proposed energy, industrial and regional integration system.

If delivered, it could support electricity generation, industrial zones, fertilizer production, mining, manufacturing and energy security across multiple African economies.

For Morocco, it would add a major southern Atlantic dimension to its energy strategy.

The 2026 Agreement Test

The pipeline has been discussed for years, but 2026 is an important checkpoint.

Officials have indicated that an intergovernmental agreement for the project could be signed in 2026, following feasibility and engineering work. Recent industry reporting has described the project as having completed feasibility and FEED phases, with a targeted intergovernmental agreement expected this year. (Maritime Professional)

That matters because the project’s next phase is not only technical.

It is political, legal and financial.

A pipeline crossing multiple jurisdictions requires agreements on transit rights, tariffs, gas volumes, environmental rules, ownership, financing, security, operation and dispute resolution.

The intergovernmental agreement would not make the project inevitable.

But it would mark a shift from concept toward formal execution architecture.

For investors, the agreement is one of the first real tests of bankability.

Why the Project Matters for Morocco

For Morocco, the pipeline fits into several long-term priorities.

Energy diversification. Morocco has worked to reduce dependence on coal while expanding renewable energy. Gas can provide flexibility for power generation and industry.

Industrial competitiveness. Reliable gas supply could support industrial zones, fertilizers, manufacturing and export-oriented production.

Atlantic strategy. The pipeline would reinforce Morocco’s role along the Atlantic corridor, complementing projects such as Dakhla Atlantique and other southern development initiatives.

Africa-Europe positioning. The project could strengthen Morocco’s role as a platform connecting African energy resources with regional and European markets.

Energy security. Diversified gas access would improve resilience, especially as global energy markets remain volatile.

This is why the pipeline is strategically important.

It aligns with Morocco’s broader effort to connect infrastructure, energy, trade and regional integration into a single development model.

Why It Matters for West Africa

The pipeline’s impact would not be limited to Morocco.

For West African countries along the route, the project could provide access to gas for power generation, industrial development and domestic energy markets.

That matters because energy reliability remains one of the major constraints on industrialisation across the region.

If gas supply becomes more accessible, it could support:

- electricity generation

- fertilizer production

- mining and processing

- industrial zones

- cement and heavy industry

- urban energy demand

- regional energy trade

The project could also strengthen regional integration by linking energy systems across the Atlantic coast.

But the benefits would depend on how the pipeline is structured.

If the project mainly serves transit and export markets, local development benefits could be limited. If it supports domestic offtake and industrial use along the route, the economic impact could be much broader.

That will be one of the central policy questions.

The Europe Dimension

Europe is another part of the pipeline’s strategic logic.

The continent continues to diversify energy supply routes after years of volatility in global gas markets.

A pipeline connecting Nigerian gas through Morocco could, in theory, create another supply option into European markets.

But Europe’s role must be understood carefully.

This is not a short-term energy fix.

A project of this size would take years to finance, build and commission. By the time it becomes operational, Europe’s energy mix may be different, with more renewables, LNG infrastructure, storage and hydrogen-related systems.

That does not eliminate the project’s relevance.

It changes the underwriting question.

The pipeline must be commercially viable in a world where gas remains important for flexibility, industry and transition energy — but where long-term carbon policies are becoming stricter.

For Morocco and Nigeria, the challenge is to align the pipeline with both energy security and the energy transition.

The Financing Challenge

The biggest challenge is financing.

At an estimated $25 billion, the Nigeria–Morocco Gas Pipeline would require one of the most complex financing structures in African infrastructure.

The project would need support from governments, development finance institutions, export credit agencies, commercial lenders, energy companies and possibly sovereign investors.

But financiers will not evaluate the project on strategic ambition alone.

They will look for:

- bankable offtake agreements

- creditworthy buyers

- clear tariff structures

- political risk mitigation

- security risk management

- environmental and social compliance

- construction guarantees

- regional legal agreements

- long-term gas supply commitments

In other words, the project must become financeable, not only strategic.

That is the difference between a historic vision and a bankable infrastructure asset.

The Security and Jurisdiction Risk

A pipeline crossing multiple countries carries a risk profile very different from a single-country project.

The Nigeria–Morocco route would involve multiple jurisdictions along the Atlantic corridor. Each adds legal, regulatory, political and security complexity.

The project must manage:

- transit agreements

- cross-border regulation

- maritime and onshore routing

- security of infrastructure

- community and land issues

- environmental approvals

- country-by-country permitting

- operator coordination

Security and jurisdiction risk will be among the most important underwriting issues.

A pipeline is only as reliable as its weakest link.

For investors, that means the project’s bankability depends not only on engineering, but also on regional coordination.

Morocco’s Gas Infrastructure Question

The pipeline also intersects with Morocco’s own gas infrastructure planning.

Morocco has been working on LNG and pipeline infrastructure linked to Nador West Med, including a planned floating LNG terminal and connections to existing gas infrastructure. Reuters reported in February 2026 that Morocco’s energy ministry paused tenders for a Nador West Med LNG terminal and related pipeline projects, citing “new parameters and assumptions.” (Reuters)

This does not undermine the Nigeria–Morocco pipeline.

But it shows that Morocco’s gas infrastructure strategy is still evolving.

For the Nigeria–Morocco project to become fully effective, Morocco will need a clear domestic gas network, import/export infrastructure, power-sector integration and industrial offtake planning.

The pipeline cannot exist in isolation.

It must connect into a wider energy system.

That makes Morocco’s domestic gas infrastructure one of the key execution variables.

Industrialisation and the Gas Transition

Gas can play an important role in Morocco’s industrial future.

It can support power generation, industrial heat, fertilizers, heavy industry and backup flexibility for renewable energy systems.

That matters because Morocco is trying to expand export-oriented manufacturing, green industry and large-scale infrastructure.

But gas also sits in a changing energy landscape.

Renewables are becoming cheaper, carbon regulation is tightening and long-term investors are more sensitive to climate exposure.

The Nigeria–Morocco pipeline therefore needs to be positioned carefully.

Its strongest argument is not that gas replaces clean energy.

Its strongest argument is that gas can support industrial transition, grid flexibility and regional energy access while renewable capacity expands.

That makes the project part of a transition framework — not a contradiction to Morocco’s renewable ambitions.

How the Pipeline Fits Morocco’s Atlantic Strategy

The pipeline also connects with Morocco’s broader Atlantic strategy.

Dakhla Atlantique, southern development projects, port expansion, fisheries infrastructure and West Africa-facing logistics all point toward a stronger Moroccan focus on the Atlantic corridor.

The Nigeria–Morocco pipeline would add an energy backbone to that same geography.

If aligned properly, Morocco’s Atlantic strategy could include:

- ports

- logistics

- fisheries

- industrial zones

- energy corridors

- West Africa-facing trade

- southern regional development

That would make the pipeline more than an energy project.

It would become part of a wider Atlantic economic architecture.

The risk is fragmentation.

If port, energy, industrial and regional projects develop separately, the impact will be weaker. If they connect, the strategic value increases significantly.

MMO Nigeria–Morocco Gas Pipeline Dashboard: 2026

Project scale

Strategic upside: approximately 6,800 to 6,900 kilometres of pipeline infrastructure with potential capacity around 30 bcm per year.

Execution risk: extreme complexity across multiple jurisdictions, landscapes and regulatory systems.

Investor test: can the project move from technical feasibility to legally binding execution agreements?

Financing

Strategic upside: one of Africa’s most transformative energy infrastructure assets.

Execution risk: estimated cost around $25 billion, requiring major multi-source financing.

Investor test: are offtake agreements, tariffs, guarantees and political-risk protections bankable?

West African energy access

Strategic upside: potential gas supply for power generation and industry across the Atlantic corridor.

Execution risk: benefits depend on domestic offtake, not only transit.

Investor test: do countries along the route secure usable energy access and industrial demand?

Morocco energy security

Strategic upside: diversified gas access and stronger role as an energy platform.

Execution risk: Morocco’s domestic gas infrastructure and LNG planning remain in transition.

Investor test: is there a clear network for power plants, industry, storage and export connections?

Europe-facing optionality

Strategic upside: potential long-term gas route toward European markets.

Execution risk: Europe’s carbon policy and energy transition may reshape gas demand by the time the project is operational.

Investor test: is the project viable under future European energy and carbon rules?

Regional security and coordination

Strategic upside: deeper regional integration and shared infrastructure.

Execution risk: cross-border security, permitting, transit rights and governance complexity.

Investor test: are legal and operational responsibilities clearly allocated across the route?

What This Means for Investors and Businesses

The Nigeria–Morocco Gas Pipeline could create opportunities across energy, construction, engineering, power generation, industrial zones, fertilizer, logistics, finance and regional trade.

But it should not be evaluated like a normal infrastructure project.

It is a multi-country energy corridor.

Investors and businesses should focus on several questions:

Is the intergovernmental agreement signed and enforceable?

Are gas volumes and offtake commitments secured?

Which countries along the route will receive usable supply?

How will tariffs be structured?

Who finances construction and who carries political risk?

How will security risk be managed across the corridor?

How does the project align with Morocco’s LNG and domestic gas infrastructure?

Can the pipeline remain viable under future carbon and energy-transition rules?

These questions matter because the project’s strategic value is enormous, but so is the execution burden.

Final Perspective

The Nigeria–Morocco Gas Pipeline is one of the most ambitious infrastructure visions in Africa.

If delivered, it could connect Nigerian gas resources to West African markets, Morocco and potentially Europe, while supporting energy security, industrial development and regional integration.

For Morocco, it would reinforce the country’s Atlantic strategy and strengthen its role as a platform between Africa and Europe.

But the pipeline’s success will not be determined by diplomacy alone.

It will depend on financing, offtake agreements, security, engineering, domestic gas infrastructure, regional governance and long-term energy demand.

Gas creates the resource base. Infrastructure creates the corridor. Finance creates bankability. Execution creates reality.

That is the real test of the Nigeria–Morocco Gas Pipeline.