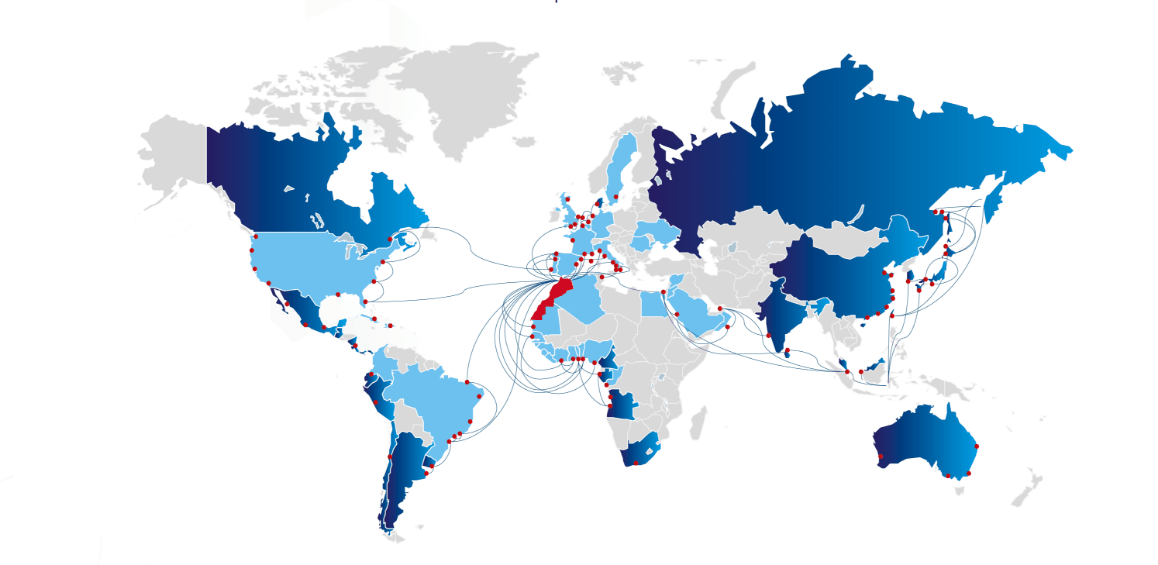

Morocco’s strategic value in 2026 is no longer defined by geography alone.

The country sits between Europe, Africa and the Middle East, but its importance increasingly comes from how it operates across all three systems at once: European supply chains, African expansion markets and Gulf-linked capital flows.

That positioning gives Morocco a rare geo-economic profile.

It is close enough to Europe to serve as a nearshoring and export platform. It is connected enough to Africa to support regional expansion. It is open enough to Gulf and Middle Eastern investment to attract capital into infrastructure, tourism, energy and real estate.

For Morocco, the opportunity is clear: turn multi-regional access into economic leverage.

For investors, the question is sharper: can Morocco balance these three relationships without overdependence on any single one?

The Multi-Regional Thesis

Morocco’s economic strategy is built around a three-layer model.

Europe provides demand.

Africa provides expansion.

The Middle East and Gulf provide capital.

Few markets can operate across those three layers at the same time.

Morocco’s advantage is not simply that it is located between regions. It is that the country has built infrastructure, trade relationships, investment frameworks and corporate networks that allow it to participate in several regional systems simultaneously.

That makes Morocco more than a bridge.

It makes it a multi-regional platform.

The strategic value comes from balance. The execution risk comes from managing complexity.

Europe: The Demand Anchor

Europe remains Morocco’s most important economic partner.

The European Union is Morocco’s largest trade partner, accounting for a major share of Morocco’s external trade. EU-Morocco trade in goods reached about €60.6 billion in 2024, making Morocco the EU’s largest trading partner in the southern neighbourhood. (eeas.europa.eu)

That relationship is structurally important.

Europe provides demand for Moroccan automotive exports, agricultural products, textiles, electrical equipment, aerospace components and industrial goods. It also gives Morocco a nearby market for nearshoring, supply-chain diversification and industrial integration.

But the relationship is changing.

European companies are no longer looking only for lower-cost production. They are looking for shorter supply chains, carbon compliance, energy security and operational resilience.

That shift benefits Morocco if the country can meet the standards that European supply chains increasingly require.

The opportunity is to become a Europe-linked industrial platform.

The risk is that proximity without compliance is no longer enough.

CBAM and the New Rules of Proximity

Morocco’s proximity to Europe gives it an advantage, but carbon regulation is changing what that advantage means.

The European Union’s Carbon Border Adjustment Mechanism entered its definitive phase in 2026 after the transitional reporting period from 2023 to 2025. For exporters into Europe, this means carbon exposure is becoming part of the trade equation.

For Morocco, the implications are significant.

Industrial exporters serving Europe will increasingly need to demonstrate cleaner energy sourcing, emissions reporting and compliance readiness. That makes renewable energy, grid reliability and industrial carbon accounting part of Morocco’s competitiveness.

The country’s renewable energy ambitions therefore carry strategic trade value.

If Morocco can align industrial production with lower-carbon energy, it strengthens its position in European supply chains. If not, parts of its export base may face rising compliance pressure.

In 2026, Morocco’s European advantage is no longer measured only in kilometres. It is measured in compliance capacity.

Africa: The Expansion Layer

Morocco’s second strategic layer is Africa.

Over the past decade, Moroccan banks, insurers, telecoms, construction groups, fertilizer companies and service providers have expanded across West and Central Africa. This corporate footprint gives Morocco a role beyond North Africa.

For investors, Morocco can function as a platform for African expansion rather than only a domestic market.

That matters because Africa’s long-term growth story is increasingly tied to urbanisation, infrastructure demand, food security, financial services, logistics and industrial development.

Morocco’s advantage is that it already has corporate channels, banking relationships and institutional experience in several African markets.

The African Continental Free Trade Area adds another layer. As AfCFTA implementation deepens, rules of origin and preferential tariff frameworks could make production structure more important for companies targeting African markets.

That gives Morocco a potential dual role:

A nearshoring base for Europe.

A rules-of-origin and expansion platform for Africa.

The opportunity is powerful.

But African expansion is not automatic. It requires regulatory knowledge, local partnerships, financing capacity and country-by-country execution.

Middle East and Gulf Capital: The Financing Layer

Morocco’s third strategic layer is capital from the Middle East and Gulf.

Gulf and Middle Eastern investors have long shown interest in Moroccan real estate, tourism, infrastructure, energy and hospitality. That capital layer matters because Morocco’s development model is capital-intensive.

Airports, ports, tourism assets, renewable energy, desalination, green hydrogen, industrial zones and urban expansion all require long-term funding.

The “Morocco Offer” for green hydrogen is one example of how the country is positioning itself for international capital across renewable energy, infrastructure and industrial value chains. Moroccan authorities have framed the offer as a mechanism to support investment in renewable energy, desalination, green hydrogen and related derivatives. (maroc.ma)

For Gulf capital, Morocco offers several attractions:

political stability

proximity to Europe

tourism and real estate potential

renewable energy resources

African expansion optionality

But capital inflows also need disciplined execution.

The success of Gulf and Middle Eastern investment in Morocco depends on project bankability, land access, utility readiness, regulatory clarity and long-term demand.

Capital can accelerate development. It cannot replace execution.

The Three-Layer Strategic Model

Morocco’s multi-regional position can be understood through three layers.

Europe — Demand and Compliance

Strategic value: export markets, industrial integration, nearshoring, supply-chain resilience.

Key opportunity: Morocco can position itself as a nearby, lower-carbon production base for European companies.

Core risk: CBAM exposure, European demand cycles and technical compliance requirements.

Africa — Expansion and Scale

Strategic value: market growth, financial services, infrastructure, food security, industrial expansion.

Key opportunity: Morocco can serve as a corporate and manufacturing platform into African markets.

Core risk: fragmented regulation, uneven AfCFTA implementation and country-specific execution challenges.

Middle East and Gulf — Capital and Project Finance

Strategic value: long-term capital, infrastructure finance, tourism investment, renewable energy and real estate development.

Key opportunity: Morocco can attract capital into projects tied to energy transition, tourism, logistics and urban development.

Core risk: projects marketed on strategic narratives rather than bankable demand or delivery capacity.

Why This Matters in 2026

The global economy is becoming more regionalised.

Companies are reassessing where they produce, where they source, how they manage carbon exposure and how they reduce geopolitical and logistics risk.

Investors are also looking for markets that can connect multiple regions without being fully dependent on one.

Morocco benefits from that shift.

Its European links provide demand. Its African networks provide expansion. Its Gulf relationships can provide capital. Its infrastructure gives the model operating credibility.

But this also makes the country’s strategy more complex.

Morocco must manage different expectations from each region:

Europe wants compliance and reliability.

Africa requires adaptation and local execution.

Gulf investors demand bankable projects and long-term returns.

Balancing those expectations is now part of Morocco’s strategic challenge.

The Strategic Corridors Behind the Positioning

Morocco’s multi-regional role is not theoretical. It is supported by operating corridors.

Tangier-Tetouan-Al Hoceima. The Europe-facing logistics and export corridor, anchored by Tanger Med and industrial manufacturing.

Kenitra. The automotive and electric mobility corridor, tied to Atlantic Free Zone and Europe-linked supply chains.

Casablanca-Nouaceur. The corporate, aerospace, financial and services platform.

Rabat-Casablanca Axis. The institutional, regulatory and professional services corridor.

Agadir and southern corridors. Agribusiness, fisheries, tourism and Atlantic-facing trade.

These corridors determine where Morocco’s strategic positioning becomes economically actionable.

For investors, the question is not only whether Morocco connects regions. It is which corridor connects their business model to the right market.

The Risks Behind the Strategic Balance

Morocco’s multi-regional strategy is credible, but it carries risks.

European concentration. Morocco’s deep integration with Europe is a strength, but also a dependency. A slowdown in European demand can affect exports, manufacturing and tourism.

Carbon compliance. Europe-linked exporters must manage CBAM, emissions reporting and energy sourcing.

African execution risk. Expansion into African markets requires local knowledge, financing, regulation and operational patience.

Capital allocation risk. Gulf and Middle Eastern capital can accelerate projects, but poor underwriting can lead to overbuilt assets or speculative pricing.

Infrastructure bottlenecks. Ports, airports, utilities, land and logistics corridors must keep pace with ambition.

Water and energy constraints. Industrial development, tourism and green hydrogen all require long-term planning around water and power.

Administrative coordination. Multi-regional strategy requires domestic execution across ministries, CRIs, local authorities and project operators.

These risks do not undermine Morocco’s position.

They define the execution tests that will determine whether the position becomes durable.

MMO Strategic Positioning Dashboard: 2026

Europe layer

Role: demand anchor and industrial integration base.

Upside: nearshoring, supply-chain resilience and export access.

Risk: CBAM exposure, European demand cycles and compliance pressure.

Investor test: can the project meet EU-grade quality, carbon and delivery requirements?

Africa layer

Role: expansion platform into growth markets.

Upside: banking, infrastructure, agribusiness, services and manufacturing optionality.

Risk: fragmented regulation, uneven AfCFTA implementation and country-specific execution.

Investor test: does the business have local partners, financing capacity and regulatory clarity?

Middle East and Gulf layer

Role: capital and project-finance channel.

Upside: funding for infrastructure, tourism, renewable energy, real estate and green hydrogen.

Risk: capital deployed into projects with weak demand or execution capacity.

Investor test: is the project bankable beyond the strategic narrative?

Domestic execution layer

Role: turns external positioning into actual economic output.

Upside: infrastructure, industrial zones, incentives and institutional reform.

Risk: permitting, land, utilities, water, talent and coordination bottlenecks.

Investor test: does the local operating environment support the strategy on paper?

What This Means for Investors and Businesses

Morocco’s strategic position is valuable because it gives companies access to multiple economic systems from one base.

But serious investors should not treat that access as automatic.

The relevant questions are practical:

Is the business Europe-facing, Africa-facing or capital-project driven?

Which Moroccan corridor best supports that strategy?

Does the project depend on EU compliance, AfCFTA rules, Gulf financing or all three?

Are land, utilities, water and administrative approvals aligned with the plan?

Is demand structural, or is it based on strategic branding?

Morocco’s multi-regional advantage is strongest when external access meets domestic execution.

That is the difference between strategic positioning and investable positioning.

Final Perspective

Morocco is no longer defined by belonging to one region.

It is increasingly defined by its ability to operate across several at once.

Europe provides demand. Africa provides expansion. The Middle East and Gulf provide capital. Morocco’s challenge is to convert those layers into durable economic output.

The opportunity is significant.

But the model depends on balance, discipline and execution.

Position creates access. Balance creates resilience. Execution creates strategic relevance.

That is Morocco’s real test in 2026.